How FIRPTA Can Tie Up Your Real Estate Sale Proceeds

For many sellers, closing is the moment when months of planning finally turn into net proceeds.

But for some sellers, a large portion of those proceeds may be withheld at closing under a federal rule known as FIRPTA.

If that happens late in the transaction, it can come as a major shock.

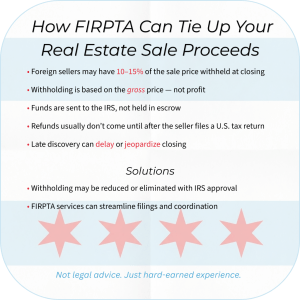

In plain English, FIRPTA can cause 10% to 15% of the sale price to be withheld and sent to the IRS, even before the seller’s final tax liability is determined. In some cases, that money may not come back until after the seller files a U.S. tax return.

That is why FIRPTA often becomes more of a cash-flow and timing problem than a pure tax issue.

What Is FIRPTA?

FIRPTA stands for the Foreign Investment in Real Property Tax Act.

It is a federal law that requires withholding in certain U.S. real estate transactions involving foreign sellers.

The important point for most sellers is not the acronym. The important point is this:

If FIRPTA applies, a portion of the sale proceeds may be withheld at closing.

That withholding is based on the gross sale price, not the seller’s profit.

So if a seller is expecting to receive a certain amount at closing, FIRPTA can materially reduce the amount actually available that day.

Why Sellers Are Surprised by FIRPTA

FIRPTA issues often do not show up until later in the transaction, which is why they create so much frustration.

From a seller’s point of view, the problem usually looks something like this:

- the deal is under contract

- closing is approaching

- everyone seems to be moving forward normally

- then a large withholding issue suddenly appears

At that point, the seller may learn that a meaningful percentage of the sale price is going to the IRS instead of into the seller’s account.

That surprise is what makes FIRPTA so disruptive.

FIRPTA Withholding Is Based on the Sale Price, Not Profit

One of the most misunderstood parts of FIRPTA is how the withholding amount is calculated.

It is generally based on the gross purchase price, not on:

- net proceeds

- gain

- equity

- or actual tax owed

That means the withholding can feel especially harsh in a deal where the seller does not believe the taxable gain is high, or where the seller expects little or no tax to be due.

From the seller’s perspective, this is often the moment when FIRPTA starts to feel less like a tax concept and more like a proceeds problem.

Why Sellers May Not Get the Money Back Right Away

Another major point of frustration is timing.

If FIRPTA withholding applies, those funds are not just held casually in escrow while everyone sorts things out.

They are sent to the IRS.

In many cases, the seller does not recover any over-withheld amount until after filing the appropriate U.S. tax return.

That means sellers can be left waiting well beyond closing to recover funds they expected to receive immediately.

This is why early planning matters so much.

FIRPTA Can Delay or Complicate Closing

FIRPTA does not always delay a closing, but it certainly can.

Problems often arise when:

- FIRPTA status is identified late

- expectations were not managed early

- documentation is incomplete

- the parties are trying to understand withholding at the last minute

When that happens, closings can become more stressful than they need to be.

The issue is often not whether the law exists. The issue is that the parties did not prepare for its practical impact soon enough.

Can FIRPTA Withholding Be Reduced?

Sometimes, yes.

In certain situations, withholding may be reduced or eliminated with IRS approval.

That is one reason sellers should not wait until the week of closing to think about FIRPTA. Timing matters, and in some cases, early action can help reduce over-withholding or improve coordination.

This is also why FIRPTA services and tax professionals sometimes become part of the conversation. The goal is usually not to “beat the system.” The goal is to avoid unnecessary delay, confusion, or cash-flow problems.

The Real Seller Takeaway

For sellers, FIRPTA is not just a tax topic.

It is a transaction-planning topic.

If FIRPTA applies, the practical consequences may include:

- reduced proceeds at closing

- funds sent directly to the IRS

- delayed recovery of withheld money

- more stress near closing if the issue surfaces late

That is why it helps to identify the issue early and understand the available options before the closing date is approaching.

Bottom Line

FIRPTA can tie up sale proceeds in a way many sellers do not expect.

The biggest problem is usually not the concept itself. It is the timing of the discovery and the impact on the seller’s money at closing.

When FIRPTA applies, planning early can make a major difference.

Not legal advice. Just practical insight from real estate transactions.

The post How FIRPTA Can Tie Up a Seller’s Real Estate Sale Proceeds appeared first on Real estate attorney in Chicago, Illinois.